Introduction

We’re increasingly told that artificial intelligence will replace huge numbers of workers because software scales infinitely. Once an AI model exists, the argument goes, it can simply be copied, deployed everywhere, and perform the work of humans at a fraction of the cost.

But there’s a problem with that narrative.

The calculation, as it turns out, has not yet been finished.

A 2012 survey found that 29% of Americans thought “the cloud” referred to an actual cloud in the sky — and that 51% believed bad weather could interfere with cloud computing. It sounds like a joke, but the misunderstanding is revealing — we have become remarkably good at thinking about digital infrastructure as though it has no physical presence at all. It does. The cloud is a vast network of warehouses full of servers, cooling systems, and substations consuming enormous amounts of power.

The real question may not be whether AI can replace humans technologically, but whether it can do so economically — once the full costs of infrastructure, energy, and accountability are finally internalised into the comparison.

The Infinite Scale Myth

The “scales infinitely” argument is seductive because it is partly true. Once an AI model has been built and trained, the cost of running one more query is very small. In that narrow sense, yes — software does scale in a way that humans cannot.

But one more query is not the question. The question is what it costs to replace thousands of workers’ worth of decisions, every day, indefinitely — while keeping the underlying model updated, accurate, secure, and compliant as regulations, markets, and the world change around it. Those are very different numbers.

Think of it this way. Sending a single email is essentially free. But running the infrastructure that delivers two billion emails a day is not. The marginal cost argument looks at the email and ignores the servers.

There is also a subsidy problem that tends to get overlooked. The prices companies pay for AI tools today are not necessarily the prices they will pay in five years. The major AI providers are currently burning substantial investor capital to establish market position and acquire users — both for future revenue and for the data that feeds back into training and improving their models. OpenAI, for example, is projected to lose $14 billion in 2026 alone, with cumulative losses before reaching profitability expected to approach $143 billion. What looks like an affordable subscription now may look rather different once those economics normalise and infrastructure costs are passed on in full.

Railways were also described as an infinitely scalable, transformative technology — and they were. They reshaped economies, decimated older industries, and created entirely new ones. But they still required decades of enormous capital investment, produced serious bottlenecks, and remained expensive to operate at scale. The same was true of electricity grids.

Each of them, eventually, stopped being “technology” and became infrastructure — unglamorous, capital-intensive, and subject to the same physical and economic constraints as everything else.

AI is beginning to follow the same trajectory — moving from a software mindset, where scale feels free, toward an infrastructure one, where capital intensity and energy constraints accumulate and compound. AI will almost certainly transform the economy. The real question is whether that transformation involves wholesale human replacement, and whether the economics that make that case are as clear as they currently appear.

AI Is Becoming Physical Infrastructure

The technology industry has spent decades encouraging us to think upwards — to the cloud, to the network, to the digital realm. The physical reality has always pointed downward: to the ground, to the concrete, to the grid.

AI is making that reality impossible to ignore.

The world’s largest technology companies are no longer just building software. They are becoming energy companies. Microsoft has signed deals to restart a mothballed nuclear power station. Google has contracted to develop small modular reactors. Amazon has acquired stakes in nuclear developers and purchased nuclear-powered data centre facilities outright.

These are not peripheral investments — they are strategic bets on the fact that without a guaranteed, large-scale power supply, their AI ambitions simply cannot run.

That is a remarkable signal. When a software company decides it needs to own its own electricity generation, you are no longer in the realm of software economics. You are in the realm of industrial infrastructure. It is also worth noting what these deals do not do: they do not solve an immediate power problem. Reactor construction takes an average of nine years and has historically run to cost overruns exceeding 200%.

The technology companies signing these agreements are investing in infrastructure that will come online in the next decade, not the next year.

Data centres are already among the most energy-intensive buildings ever constructed. A large facility can consume as much electricity as a small city. The International Energy Agency projects that they will consume more than 1,000 terawatt-hours of electricity in 2026 alone — roughly equivalent to Japan’s entire annual electricity consumption — and that demand from AI-optimised data centres will more than quadruple by 2030.

If these projections hold, we may hit an energy ceiling sooner than we hit an intelligence ceiling.

Electrical infrastructure in most developed countries was not designed for this kind of sudden, concentrated demand. In the United Kingdom alone, grid connection applications surged by 460% in just six months, driven predominantly by data centres. Grid connection approvals take three to eight years; a data centre can be built in eighteen to twenty-four months.

This is not a problem confined to industrial megaprojects. When our own firm relocated its offices — moving, quite literally, one door down the same street — the single largest source of delay had nothing to do with leases, fit-out, or logistics. It was waiting for an electricity supply connection. That took seven months. The physical move took a weekend. If a small office relocation can be held up for the better part of a year by the pace of grid infrastructure, the idea that vast new data centre campuses will be energised on a developer’s preferred timeline deserves careful scrutiny.

The gap between building capacity and powering it is, at this moment, structural. Transformers — the hardware that steps power up and down across the network — face severe global supply shortages. In some parts of the United States and Europe, data centre developers are already being told they cannot connect new facilities because the local grid simply cannot absorb the load.

And AI is not the only pressure bearing down on that infrastructure. The transition to electric vehicles represents the other major demand shock hitting grids at exactly the same time. Report after report has concluded that most national grids are nowhere near ready for a full shift to electric motoring. If grids are struggling to prepare for the cars, it is worth asking how ready they are for the data centres.

The vision of AI seamlessly absorbing the work of millions of people assumes that the infrastructure to run it at that scale either already exists or can be built quickly. Neither assumption is certain.

The Economics at Scale

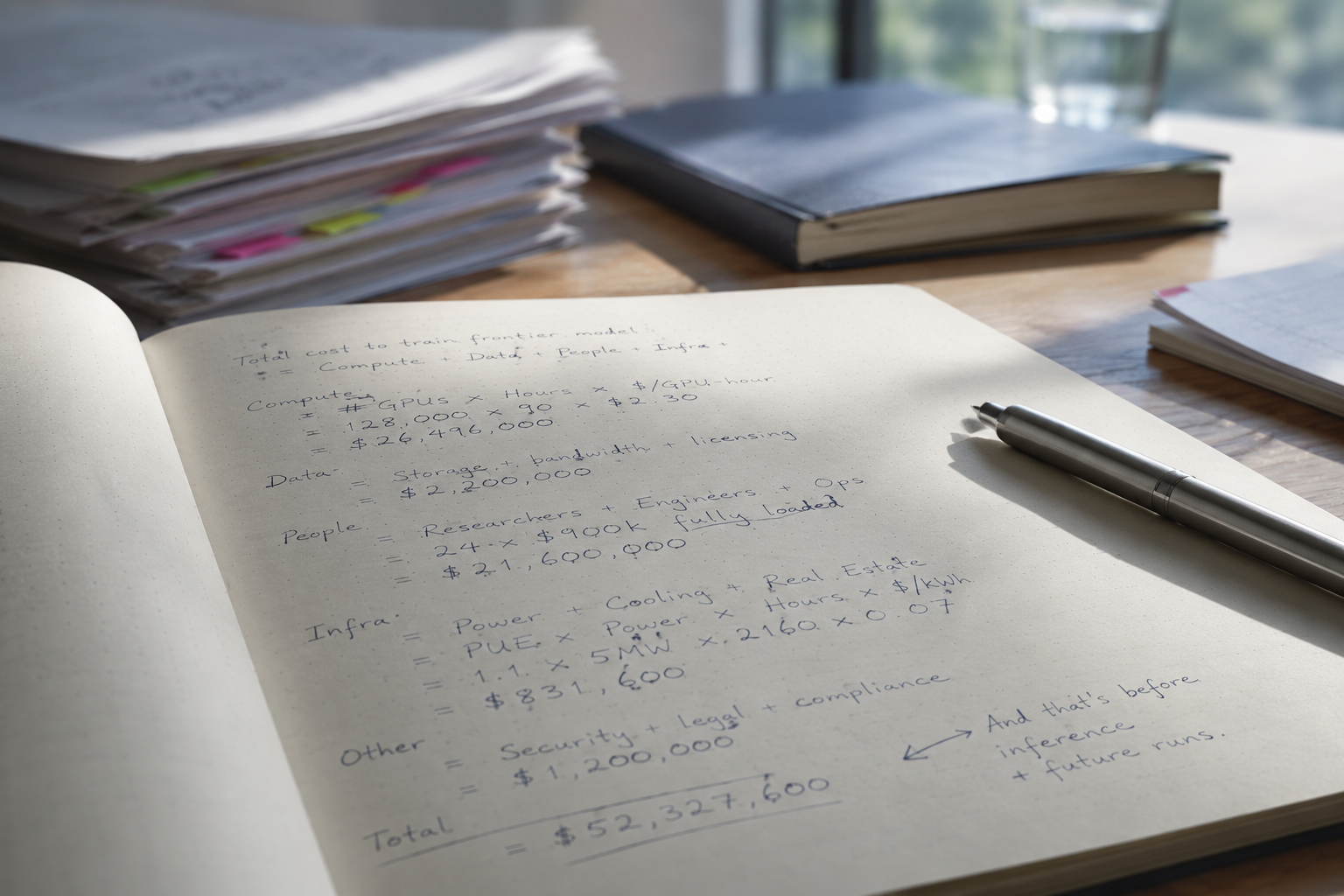

Set the infrastructure questions aside for a moment and consider a simpler one: when a business replaces a human worker with an AI system, what exactly does it cost?

A human employee is expensive in ways that are visible and well understood. Salary, benefits, pension contributions, office space, training — these figures are measured in the P&L, tracked year on year, and easily compared with alternatives as they arise. The cost of replacing that person with AI looks, at first glance, highly attractive. A standard subscription package is a single line item. It is easy to imagine the saving.

In practice, businesses face one of two routes: building or deploying their own models, or subscribing to a platform provided by one of the major AI companies. The economics of each look quite different — though perhaps not in the ways most business cases currently assume.

For those building or deploying their own models — running private infrastructure, training on proprietary data, operating at scale within their own environment — the costs of compute, energy, hardware, maintenance, and cybersecurity fall directly on them. These businesses are, in effect, becoming small-scale versions of the AI providers themselves, with all the infrastructure burden that entails. Add to that the cost of downtime — in a fully automated operation, no longer a minor inconvenience but a business-critical event. And unlike a human employee, an AI system does not update itself; models require ongoing retraining as the world changes, at a cost that rarely features in initial projections.

There is a further complication that matters regardless of whether you are self-deploying or taking an off-the-shelf subscription. Energy markets have not yet fully repriced around AI demand. The cost of running compute-intensive workloads at scale is, at this moment, artificially low relative to what it will likely be in a decade when demand has fully materialised and infrastructure investment is being recovered.

The immediate cost of a subscription may look manageable — but the providers behind those subscriptions are carrying enormous and growing infrastructure costs of their own. The world’s largest AI companies collectively spent more than $400 billion on capital expenditure in 2025, a figure expected to rise by a further 75% in 2026.

Those costs will not be absorbed indefinitely. As energy prices rise and investor subsidies normalise, those costs will find their way into the price of the subscription. The businesses that have built workforce strategies around today’s pricing should plan accordingly.

None of this appears in the headline subscription price. Most of it does not appear in the business cases being written today.

Bryan Catanzaro, Vice President of Applied Deep Learning at Nvidia — the company whose chips power the industry — put it plainly in an interview with Axios: “For my team, the cost of compute is far beyond the costs of the employees.”

When the hardware supplier is saying this, business cases built on the assumption that AI is simply cheaper than people deserve a second look.

The economics of AI adoption are not unfavourable — in many cases they are genuinely compelling. But the argument that AI is simply cheaper than people, and therefore will straightforwardly replace them, is a comparison that only holds if you look at a narrow slice of the cost picture. Research from MIT has found that even in the category of tasks where AI is technically capable of automation, deployment costs make it economically viable in only a minority of cases.

Technical capability and economic viability are not the same thing. The full picture is considerably more complicated.

The Energy Problem Underneath Everything

AI models are becoming more efficient all the time. Inference costs are falling rapidly — the cost of running a model at GPT-4 level capability has fallen by a factor of rougly one hundred since 2023. Researchers are finding ways to do more with less compute. Surely, as the technology matures, the energy and infrastructure burden will shrink rather than grow?

It is a reasonable argument. It is also, at the level of total demand, historically quite wrong — and there is an economic principle that explains why.

In 1865, the English economist William Stanley Jevons observed something counterintuitive about the steam engine: as it became more fuel-efficient — by a factor of roughly eight — coal consumption did not fall. It increased eighteen-fold over the following decades.

Cheaper, more efficient energy use did not reduce demand — it expanded it, by making coal-powered activity viable in new contexts and at greater scale. The economic principle that bears his name — Jevons Paradox — has since been observed across industry after industry. Cars became more fuel-efficient; people drove more. Computing became cheaper; we used vastly more of it. Efficiency improvements did not reduce total consumption. They unlocked it.

Jevons Paradox operates at the demand level. There is little reason to think AI will be different. If the cost of running AI falls by a factor of ten, the likely response is not that companies spend a tenth as much on AI. It is that they find ten times as many uses for it. Every task that was previously marginal becomes viable. Every workflow that was partially automated becomes fully automated. The demand expands to fill — and exceed — whatever efficiency gains the engineers achieve. We may build far more efficient models and still consume far more energy overall.

But Jevons only tells part of the story. Usually, when we talk about energy and AI, we focus on consumption — on running the models, cooling the data centres, keeping the lights on in the server farms. What we rarely discuss is everything that happens up until the point of consumption.

Consider what it actually takes to build the hardware that AI runs on. Minerals are extracted from mines in the Democratic Republic of Congo, Chile, and Australia. They are refined and processed, then manufactured into chips in extraordinarily energy-intensive fabrication plants in Taiwan and South Korea. Those chips are shipped globally, assembled into servers, and installed in data centres that will consume electricity continuously for years to come. Every stage in that chain consumes energy. Every stage also has a geography, and a politics.

All of this before a single query is ever run. From mining minerals to mining crypto to mining databases — energy is present at every step, in quantities that conventional technology cost models rarely capture.

And threading through all of it is a geopolitical reality that deserves to be named directly. The majority of rare earth processing runs through China. The overwhelming majority of advanced chip fabrication runs through Taiwan. Readers will draw their own conclusions about the risk profile of a supply chain that concentrated. What can be said plainly is that a concentrated supply chain cannot be assumed to be a resilient one — and any serious disruption, political or otherwise, would constrain global AI capacity in ways that no amount of software optimisation could compensate for. The energy and infrastructure story is, quietly, also a story about where in the world the physical prerequisites for AI actually sit.

Does that mean efficiency gains count for nothing? Not quite — but they work differently than most assume. Jevons tells us efficiency won’t reduce total demand. What efficiency improvements can do is help stem the bleeding in the short term: by reducing how much energy each unit of AI workload requires, they buy time while grids are upgraded, new power capacity is built, and infrastructure catches up with adoption. Software can improve in months; power stations take years to build. If AI models become dramatically more efficient during that window, the gap between what the grid can deliver and what AI demands may remain manageable. Whether efficiency gains can run fast enough and for long enough to bridge that gap is genuinely uncertain — but it is the most plausible version of the optimistic case.

Efficiency improvements help, but they do not resolve the underlying problem. Software capability grows in months. Power stations and grid infrastructure are built over years and decades. Until energy production and deployment can scale at anything approaching the pace of the software it is being asked to support, there will be a structural gap between what AI can do and what the infrastructure can sustain. Efficiency can narrow that gap. It cannot close it alone.

The Case for Humans

Amid all of this — the energy demands, the supply chains, the infrastructure gaps — it is worth pausing on a rather basic observation: the human brain runs on roughly 20 watts. About the same as a dim lightbulb. Some lightbulbs, it must be said, are dimmer than others — but even accounting for that, the human brain remains one of the most energy-efficient information-processing systems ever produced. It runs on caffeine, crisps, and the occasional vegetable. No mining required. No shipping container. No substation.

This is not a trivial point. When we discuss replacing human workers with AI systems, we rarely factor in that human beings arrive ready to work and carry essentially no incremental infrastructure cost. They were going to eat lunch anyway. Nobody built roads so they could commute to work — the roads were already there. Nobody constructed housing so they could turn up on Monday morning — the houses were already there. The infrastructure that supports a human worker at their desk was built, financed, and largely paid for by society long before any employer needed it. In non-manual roles especially, the marginal cost of a person arriving and doing their job — in energy, capital, and logistics terms — is almost nothing. Stack that against the supply chain described above and the comparison looks rather different.

That covers the physical side of the ledger. The stronger case for humans sits in territory that resists quantification entirely: trust, judgement, and the quality with the hardest edges — accountability.

Consider the driverless car. The astrophysicist Neil deGrasse Tyson has argued compellingly that fully autonomous vehicles would save enormous numbers of lives — and the logic is straightforward. In Northern Ireland alone, around 60 to 70 people die on the roads every year.

If AI-driven vehicles reduced that figure to five or six, it would represent one of the most significant public safety achievements in decades. Tyson’s point is that society may simply lack the patience — or the courage — to accept the transition period, with all its imperfections, in order to reach that outcome.

He is almost certainly right. And the reason gets to something fundamental about how humans relate to accountability. If an autonomous vehicle kills someone’s parent, sibling, or child, the grief does not arrive with a statistical footnote explaining that overall road deaths are down 90%. It arrives as a question with no satisfying answer: who is responsible? Who do I hold to account? A software update? A product liability team? A corporation?

The same question applies across professional life. If an AI wealth management system loses everything, who answers for it? If an AI legal tool misses a critical clause and a business suffers, where does the liability sit? As a Chartered Accountant, I pay significant professional indemnity insurance premiums every year precisely because I carry personal responsibility for the advice I give. AI companies, meanwhile, point to the disclaimer on their products — “AI can make mistakes” — and consider the matter closed.

The gap between those two positions is not an abstract philosophical problem. It is a practical, legal, and deeply human one, and at the moment the answers are genuinely unclear in ways that make wholesale AI replacement of professional judgement far more complicated than the technology alone would suggest.

People take comfort in accountability. Not because humans never make mistakes — they make them constantly — but because when a human professional fails, there is a person, a regulator, a professional body, and a legal system that can respond. That infrastructure of trust and consequence has been built over centuries. AI is, in this sense, still on probation.

Over the course of a career in professional services, the range of human situations that arrive across a desk is difficult to anticipate in a business plan. I have sat with clients who discovered, sometimes in that very meeting, that they had lost their savings to a cryptocurrency scam — money they had trusted someone to protect, gone. I have had conversations with clients navigating divorce, trying to understand, in among everything else they were already carrying, what it would mean for a business they had spent years building. I have met people who were quietly going through the hardest periods of their lives, and who needed, in that moment, something that does not appear in any service description.

Here is the thing about those conversations: some of them, the client might genuinely have found easier to have with an AI. There is something about the remove of a screen, the absence of a face reading yours, that can make it easier to say the hard thing first. I do not dismiss that. But easier to start is not the same as better. An AI can process the information. It can generate a relevant answer. What it cannot do is sit with someone in distress and make them feel less alone in it. It cannot absorb what is in the room and reflect something steadier back. It cannot, in any meaningful way, care.

I had a conversation with another accountancy practice owner once, where he described what he did as “selling time for a living” — meaning, simply, that he billed for his hours. In fields where trust is the product, I never felt that was quite right — not for me, anyway. What I sold was peace of mind. Competence. Trust. I sold people their time back by taking responsibility for things I could do well for them, things they no longer had to think about or worry about. That is not a transaction that fits neatly into an AI cost model. And until it does, the case for the human professional remains stronger than the headlines suggest.

The Tax Question

There is a cost to AI-driven workforce replacement that almost nobody in the technology industry talks about, probably because it does not appear on any company’s balance sheet. It appears on the government’s.

The modern state is, in economic terms, a machine built on the assumption that large numbers of humans work. They earn wages, those wages are taxed, employers pay contributions on top, and the workers spend what remains — generating further tax through consumption. In the United Kingdom, income tax and National Insurance contributions alone raised approximately £475 billion in 2024/25, accounting for over 42% of all government receipts.

Add VAT — funded largely by consumer spending, itself funded largely by wages — and those three taxes alone raised roughly £651 billion. Over half of everything the government collects comes, directly or indirectly, from the fact that people have jobs.

In the United States, the picture is even more pronounced. Employment-linked taxation represents roughly three-quarters of federal revenue.

Now consider what happens when a company replaces a thousand workers with AI systems. From the company’s perspective, the economics may be compelling — lower headcount, higher productivity, improved margins. From the Treasury’s perspective, the picture looks rather different. A thousand fewer workers means a thousand fewer income tax contributions, a thousand fewer sets of National Insurance payments from both employee and employer, and a meaningful reduction in the consumer spending that generates VAT. The company’s profits may rise, but profits are taxed at a lower effective rate than labour, and — critically — profits are mobile in ways that wages are not. A worker in the United Kingdom pays tax in the United Kingdom. A worker in Ireland pays tax in Ireland. But a multinational can structure itself so that its profits are taxed in Ireland, Luxembourg, Estonia, Singapore, or any other low-tax jurisdiction it chooses — regardless of where the economic activity actually took place.

That asymmetry is not new, but AI threatens to make it dramatically worse. The architecture of public finances was designed for an economy in which the relationship between productivity and employment was broadly stable. More economic activity meant more jobs, which meant more tax revenue. AI breaks that assumption. It offers the possibility — for the first time at genuine scale — of rising productivity without a corresponding rise in employment. If that happens, governments face a structural funding gap that no amount of efficiency in public services can close.

The tax system, in my experience, is generally used for two things. It raises revenue for public spending. And it influences behaviour — encouraging activity the government considers beneficial and discouraging activity it considers harmful. We tax cigarettes heavily because we want people to smoke less. We give generous tax-free status to ISAs because we want people to save and invest more. These are, of course, subjective judgements that shift with whoever happens to be in government at any particular time, but the principle is well established.

In the context of AI, the interesting thing is that taxation is unlikely to arrive as a policy tool to discourage adoption. No serious government is going to try to slow down artificial intelligence through punitive taxation — the competitive consequences would be too severe. Instead, the tax will arrive for the first reason: because governments will have no choice. If employment-linked revenue falls significantly, the money to fund healthcare, pensions, education, infrastructure, policing, and defence has to come from somewhere. The question is not whether AI will be taxed. It is how, when, and how much.

Andrew Yang, the former US presidential candidate and entrepreneur, made this argument in early 2026 when he proposed dropping taxes on labour entirely and replacing the revenue with taxes on AI.

His framing was appealing — stop taxing the thing you want to keep, start taxing the thing that is displacing it. But I think he arrived at the right destination via the wrong route. The tax does not arrive because governments decide AI is bad and should be discouraged. It arrives because the bills still need to be paid. Fiscal necessity, not policy preference.

The difficulty, of course, is in the mechanism. Raising corporation tax is a blunt instrument — it increases the burden on every business, including those that have not automated at all. You end up punishing a traditional manufacturer in Belfast for a workforce decision made by a technology company in San Francisco. Taxing energy more heavily creates similar problems, penalising steel mills and chemical plants for something the tech sector caused. And any targeted tax on AI usage or compute — however elegant in theory — immediately raises the question of jurisdiction. If the United Kingdom imposes a meaningful levy on AI compute and Ireland does not, the data centres move. The revenue follows.

This is not a hypothetical problem. It is the same problem that led, over the past decade, to the most significant exercise in international tax cooperation in modern history. The OECD’s Base Erosion and Profit Shifting framework — BEPS — was born from precisely this dynamic: multinational companies exploiting gaps between national tax systems to shift profits to low-tax jurisdictions, costing governments an estimated $100 to $240 billion annually.

The response required over 140 countries to agree on coordinated rules, including a global minimum effective tax rate of 15% on large multinationals, now in force in more than fifty jurisdictions. It was slow, politically contentious, and imperfect — but it happened, because the alternative was a race to the bottom that no country could afford. In my own experience, the client conversations about relocating to lower-tax jurisdictions that were common a decade ago have largely gone quiet — when the floor is 15%, the arbitrage shrinks considerably.

AI taxation will almost certainly require the same kind of coordination. Digital Services Taxes, already adopted or proposed by roughly half of European OECD countries, offer a cautionary preview of what unilateral attempts at this problem look like in practice.

The results — fragmented rules, trade disputes, retaliatory threats — are instructive as a warning rather than a model. A durable solution will need to be multilateral, infrastructure-linked, and difficult to arbitrage. Something closer in spirit to VAT than to income tax — broad-based, automatically scaling with economic activity, and hard to avoid entirely. VAT itself would have sounded like a futuristic abstraction a century ago. The AI equivalent may sound equally unlikely now. But the economic pressure will make it inevitable.

There is an irony in all of this that ties directly back to the central argument. If governments succeed in taxing AI heavily enough to replace the employment-linked revenue they stand to lose, the effect will be to close the cost gap between human workers and AI systems. Not because AI has become less capable, but because its true cost — including the societal cost that taxation is designed to recover — will finally be reflected in the price. AI may remain technically superior in many tasks, but it will no longer be overwhelmingly cheaper. And if it is not overwhelmingly cheaper, the case for wholesale human replacement weakens considerably.

The Most Likely Outcome

AI will transform the economy profoundly. But it’s still uncertain whether it will replace humans wholesale, because the marginal cost argument looks at the email and ignores the servers, and the servers turn out to be extraordinarily expensive, physically constrained, geopolitcally exposed, and increasingly taxed.

So what does actually happen?

The disruption is already visible at the level of individual tasks — huge volumes of cognitive work are being automated right now and that will accelerate. Whether that translates into equivalent role elimination is a different, and less certain, question. Eliminating tasks does not automatically eliminate roles, particularly where those roles carry accountability, client relationships, or regulatory requirements. At the top of that chain — the leadership team and the people who actually have to put their signature to things — change will be slowest. Not because the capability isn’t there, but because nobody has yet worked out who is liable when it goes wrong. Until they do, humans stay in the room.

How far task disruption becomes role disruption will depend not just on what AI can do, but on infrastructure build pace, how liability gets assigned, how tax policy responds, and how governance evolves. The technology is, in all of this, the least uncertain variable.

The data so far supports a more measured story than either camp prefers to tell. The World Economic Forum projects a net gain of 78 million jobs globally — 170 million created against 92 million displaced — though those aggregate figures conceal the human reality of significant churn, geographic dislocation, and the need for retraining at scale.

Oxford Economics has found that AI-attributable job losses currently account for less than 5% of reported layoffs, with no clear sign yet of the productivity acceleration that displacement on the scale predicted would require. This is not evidence that serious disruption is not coming. It is evidence that it moves more slowly and more unevenly than the headline predictions suggest — and that the transition, when it comes in full, is likely to be measured in decades rather than quarters.

The most likely outcome, then, is not one hundred workers becoming zero. It is one hundred workers becoming fifteen — highly augmented, significantly more productive, working alongside systems that handle the volume while the humans handle the judgement. A small accountancy practice with AI will be able to serve the client base that once required a mid-sized firm. A legal team of five, properly augmented, will outperform a department of thirty working without it. The leverage is enormous, and it is real. But it is leverage applied to human capability, not a replacement for it. The humans do not disappear from the equation. They become the scarce, high-value component around which everything else is organised.

That distinction matters enormously, because it reshapes what industries actually look like. The professional services model — law, accounting, consulting, medicine — shifts from large partnerships built on headcount to lean, technology-intensive practices built on expertise and judgement. The people who remain are not doing the same jobs more cheaply. They are doing fundamentally different work: interpreting, advising, deciding, and carrying responsibility. The routine falls to AI. The consequential stays with humans. For clients, the experience may barely change. For the structure of the professions, it changes everything.

None of the constraints explored in this article will resolve quickly or cheaply. Energy infrastructure will improve, but on timescales that lag software adoption — costs will be passed on, and the era of artificially cheap compute will end. Supply chain dependencies on a small number of countries will be slowly reduced, but not within any planning horizon that matters to businesses making decisions today. Taxation will arrive, almost certainly through international coordination, and when it does it will close some of the cost gap between human workers and AI systems that today’s subsidised pricing has opened. These are not permanent barriers to transformation. They are the friction that attends every major technology transition — and the friction matters, because it shapes the pace and the distribution of what changes, and what does not.

Every major productivity technology in history has followed this trajectory. And in every case, society did not simply become cheaper. It became more complex, more regulated, and significantly better at extracting value from the new productive system. The end state was never the frictionless utopia that the technology’s early advocates imagined. It was something messier, more expensive, and more human.

AI will be no different. The 20-watt brain is not going to be made redundant by a technology that requires its own power stations, its own global supply chain, its own tax regime, and its own century of trust-building before society will let it operate unsupervised. What it will do — what it is already doing — is make the humans who learn to work with it extraordinarily powerful.

Over time, the machine will end up doing more of the work. But it will not slide the box of tissues across the table. It will not look someone in the eye and tell them — clearly, early enough to matter — that the path they are on could cost them dearly. It will not offer sincere congratulations when they deserve to be meant, or be the voice that says this is bad, but here is what we do next.These are not edge cases. In professional life, they are the work — the part that no subscription covers and no disclaimer accounts for. I have sat in those rooms. I have had those meetings.

The repetitive and the repeatable will fall to AI. Much of it already has, and much more will follow. What remains is not the lesser part of the work. It is the part that required a person to begin with — the rooms, the conversations, the moments that no model was ever going to handle. The calculation that omits those is not wrong because the technology is overhyped. It is wrong because it has not yet been finished.